Market Snapshot: July 2021

In summary

- Bond yields are back to January levels suggesting the inflation scare is no longer. The markets are currently positioned for inflation to be short term only.

- US Sharemarkets continue their strong run (up ~5%) maintaining their status as the world’s most expensive equity market.

- Chinese regulators toughen up across their bond, currency, and equity markets and this resulted in a significant sell-off in their equities market.

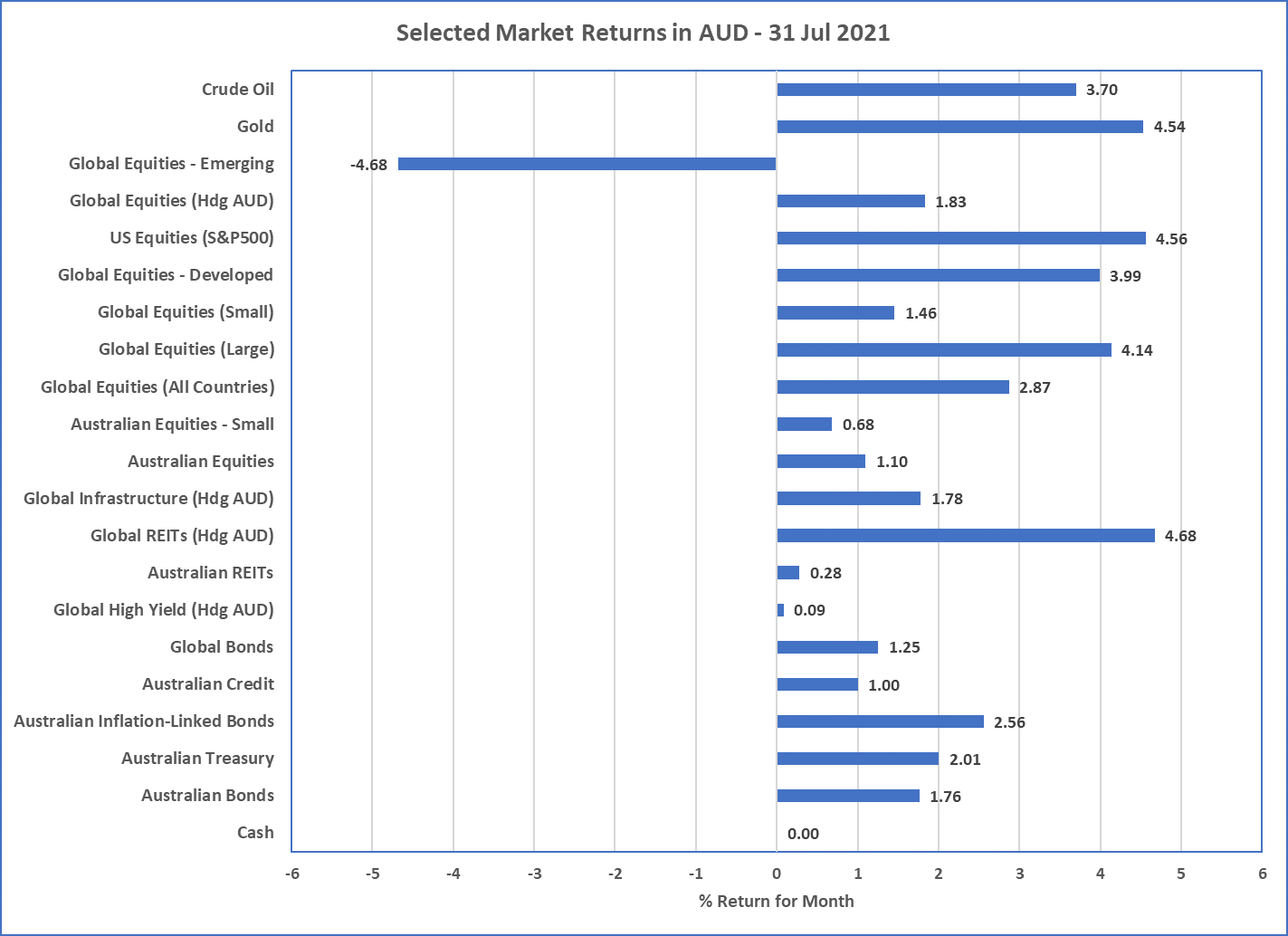

- Emerging Markets consequently was the worst performing major asset class for July down over 4%.

- The COVID lockdowns in Australia has resulted in Australia’s economic recovery stalling and will likely produce a negative GDP quarter for September 2021.

- Contrary to Australia, major economies, such as USA and Euro Area produced very strong economic growth figures for June.

- The outlook for investment returns continue very low with the only potential bright light is the risky Emerging Markets asset class.

- Portfolios continue their neutral positions across all asset classes but their defensive positioning within equities (preferred styles are Value, Quality, and Low Volatility).

Chart 1: Tough month for China and therefore Emerging Markets

Sources: Morningstar Direct

What happened in July?

Pandemic

Australia in lockdown.

- The month of July saw each mainland State capital city in Australia go into lockdown as the Delta variant created a new wave of cases and deaths. This lockdown means the economic growth for Australia will likely be negative for the September quarter and profit expectations for the equity markets will obviously be negatively affected.

- The rest of the world continues its recovery and vaccination rollout. The UK has removed its COVID restrictions which may result in stronger economic results but will it also contribute to a new variant that approaches vaccination resistance? Hopefully not.

Markets

Bond Yields drop

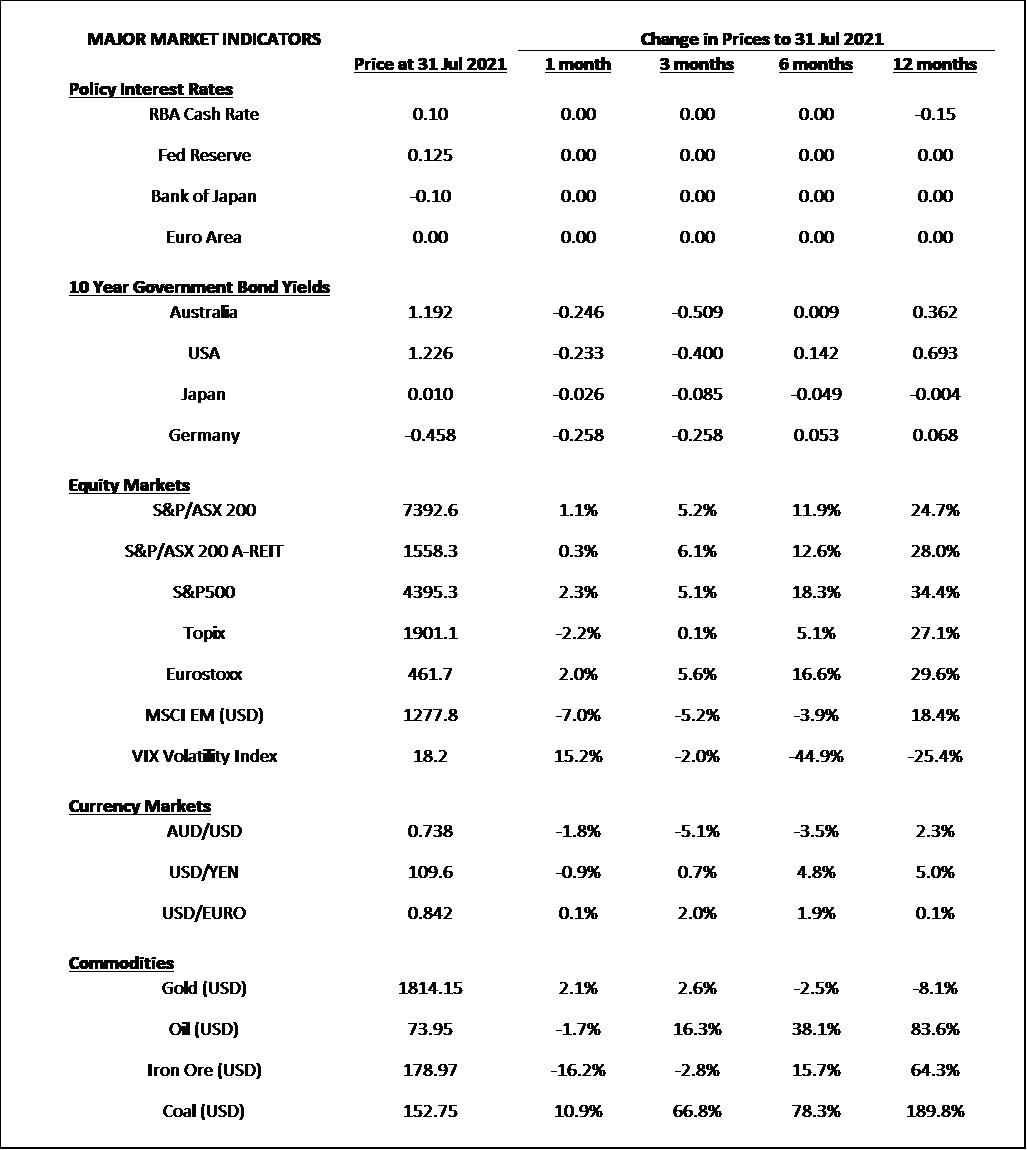

- Back in February and March, markets appeared to be concerned with higher inflation and bond yield increased massively producing the worst bond returns in many many years. That has all been revered and yields are back to January levels and it appears the inflation concerns have completely dissipated.

- From an equity market perspective, developed markets continued their charge forward with very strong results from the USA (already the most expensive market in the world), where it increased around 5% in July.

- The poor performer across all asset classes was Emerging Markets which fell almost 5% and was largely due to a big sell-off in China, particularly tech stocks, as Chinese regulators crack down on equities, bonds, and currencies and funds flow out of China from foreign investors.

Economies

Strong result from USA

- Whilst Australia’s June economic result is not due until September, the USA has reported a strong result such that the 12 month economic growth was over 12%.

- Similarly, the Euro Area has produced economic growth over the 12 months of almost 14% … this was led by France (18.7%), Italy (17.3%), and Spain (19.8%)

- As mentioned, the previous inflation fear has dissipated but the Delta Variant is showing that higher economic growth does rely on high vaccination levels and continued efficacy … so there is some time to go yet.

Outlook

With current volatility in China and high valuations in USA, and a troublesome COVID Delta variant sets the stage for a potentially more volatile second half of 2021 for risky assets.

The return outlook for all asset classes is very low and can only improve with a stronger than expected economic recovery which must be led

by a successful vaccination rollout which maintains their COVID efficacy.

Major Market Indicators

McConachie Stedman Financial Planning is an Authorised Representative of Wealth Management Matters Pty Ltd ABN 34 612 767 807 | AFSL 491619